Getting out of debt can be a trying experience. Canadians have been accumulating debt at lightning speeds, and it makes sense that we would look for ways to get out of debt just as fast. Head over to the internet and search for the hail-mary solutions late at night. Something to help climb out of any financial hole that's been created. Basically, we want the same thing for our debt plan as we do for our internet connection…we want it fast! It doesn't help that there are so many clickbait marketing tactics out there that claim that you can pay off a traditional mortgage in five to seven years using this strategy or that strategy.

However, velocity banking could be an excellent strategy to try when getting out of debt if you are willing to commit and you have the discipline to make it actually work. Oh yeah, and you need positive cash flow to even get started. It's worth noting that we're not suggesting this can be a cure-all– if you want to get out of debt, you'll have to put in the work. Velocity banking can simply help you get on the right track. By combining the habits and mindset of velocity bankers with the power of The Infinite Banking Concept, you may be able to have your cake (get out of 3rd party debt) and eat it to (build a lifelong asset). Combined, Canadians can essentially become their own banker and enjoy even more financial control and potential in their lifetime.

So what exactly is velocity banking? How does it work, and is it an ideal strategy for everyone? Let's take a look

What Is Velocity Banking?

The velocity banking strategy focuses on using a HELOC or “Home Equity Line of Credit.” It can be done with a personal life of credit as well, but in general, a readvanced HELOC is the most common method. By depositing your income into a HELOC, you are essentially cancelling interest on the periods of a month in which your money would typically be sitting collecting dust. We refer to this as an interest cancellation effect. The lender only charges you interest on an average daily balance. If your income compresses the line of credit during the lull periods of the month and sitting stagnant, you can cancel some of the interest that would otherwise accrue each day.

You can also practice the conceptual aspects of velocity banking and the habits that can make this method successful without a HELOC or personal credit line. When it comes down to it, velocity banking is all about developing the proper habits to get out of debt.

So, is velocity banking some sort of magical cure-all for paying off a mortgage in five to seven years? Unfortunately, it's not– but realistically, there is no magic way to pay off or eliminate debt other than paying that debt down. That means you still have to apply money to the principal balance you owe. No magical new money is created. Instead, your focus and attention are directed to your goal. Many will likely experience a domino effect by simplifying the process as they begin to see steady results.

The truth is that the velocity banking strategy fundamentally rests on the actions and financial behaviour of the person implementing it. Like most financial strategies and debt reduction methods, velocity banking will either work beautifully or simply fail, and the result is entirely based on the user. If you cannot follow through on your financial plan and operate with the right mindset, you will probably not receive the success you want with velocity banking. It's just like getting a gym membership– the gym membership itself won't help you lose weight, but your actions while owning that gym membership will. Saying that you do velocity banking will not eliminate your debt. The only way to truly get out of debt is to put in the work, but velocity banking can help certain families.

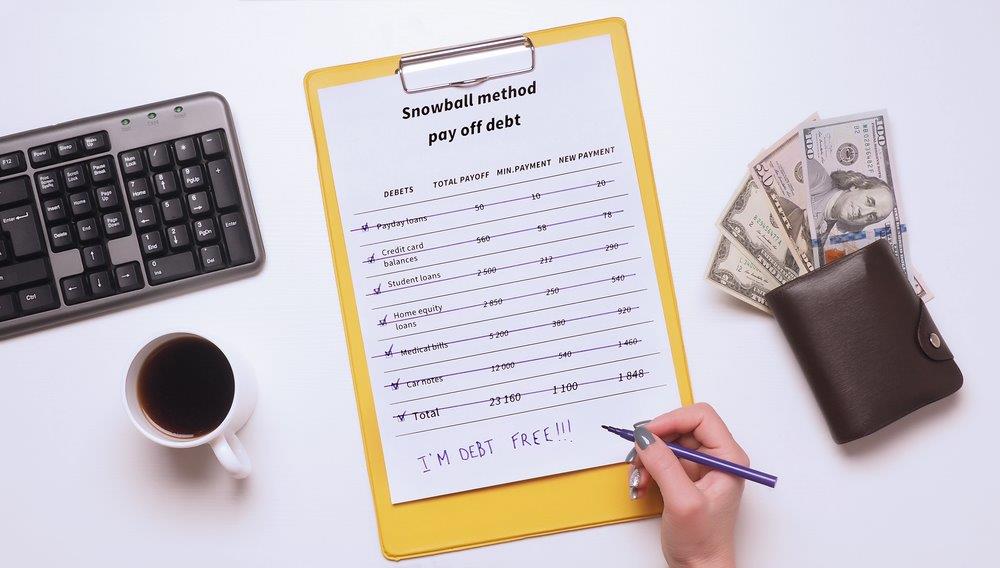

This strategy works by using a line of credit as your main account. After consistently depositing money from your pay periods and other random incomes (child tax benefit, bonuses from work, selling furniture, or tax refunds), your free cash flow reduces the balance quickly. Then strategically (without putting yourself into hot water), you can pay lump sums to pay off other debts such as credit cards and vehicle loans. Using the snowball method, those payments that used to go out every month now still sit in the HELOC, compressing it down. This compressed balance quickly grows so you can attack the big kahuna next, the mortgage. The idea here is that a line of credit will assist you in using your cash flow to cover your expenses while also going toward paying off your mortgage. There is no need for a savings account with this approach since your cash flow will go toward your debt via the line of credit or HELOC. Instead of saving on the side, you are in effect saving more due to the interest being cancelled out. For many, this is much more than any savings account with a typical bank will pay you anyhow. Typically, this approach makes it possible to pay off your mortgage faster, and the end result should be less interest paid.

A word of caution… If you get rid of the traditional mortgage portion with a fixed principal and interest payment, you have not eliminated your mortgage yet. If you have a HELOC, then you technically still have a mortgage. This is often overlooked and poorly explained by the many financial entertainers who promote this strategy. A HELOC is a pledged debt instrument against the property's title and is still considered a mortgage. Until the HELOC balance is at zero, you are not mortgage-free. With all of your cash flow freed up and no more traditional payment, the rest of the HELOC is often cleared away in record time.

Bonus for Infinite Bankers who incorporate this idea. Rather than using a HELOC, they can use the power of policy loans to rapidly recapture debt into a re-advanceable credit line using their cash value as collateral and have total control over the process.

Velocity banking calculator

A velocity banking calculator can be quite helpful in determining the timeline for your debt to be paid off. However, everyone has such a dynamic and varying financial life these calculators are typically only good for a snapshot view. They generally do not match with the daily ebb and flow of your monthly budget. You will need to know your current interest rates, minimum payments, free cash flow (positive cash flow), your initial debt amounts, and your current amortization on any amortized debts such as a mortgage. The more accurate you can be with this information, the better assessment you can get when considering a plan like this.

Velocity banking pros and cons

Velocity Banking Pros

If you are disciplined and have some disposable income, velocity banking can be an excellent way to get out of debt.

You can decrease your debt a bit quicker than with other strategies if you put the work in and stick to it.

If you have multiple debt payments leaving your household, you may find you can increase your velocity as these payments drain cash flow. Once you redirect one, then your snowball impact can amplify with each amount you reclaim in your budget. This method is all about focusing on cash flow more effectively.

Getting out of debt can really liberate you and create a new level of peace and happiness in your life. Reduced stress often means better long-term health, and you may even find a positive impact in your personal relationships as you have a newfound confidence.

Velocity Banking Cons

Accessing a line of credit can lead to more debt. Essentially, it's a slippery slope. If you have an income change like a job loss due to the pandemic, this can go sideways quickly as you tap into the line of credit to fund your life… Having access to your equity can increase purchasing. As people, we are often distracted by shiny objects. If you think this could happen to you, make sure you work with a good coach and be accountable for your decisions.

Advantages of Velocity Banking

Paying down your mortgage and other debt can save you thousands of dollars in interest.

It can help you retire earlier and have better financial independence.

You’ll improve your monthly cash flow and cash availability which can be harnessed very effectively.

Many who practice the infinite banking concept finds that this allows them to quickly increase their capital pool for future opportunities

Disadvantages of Velocity Banking

As it currently stands, mortgage interest is at an all-time low.

You may have to deal with adjustable rates for your HELOC or personal line of credit, as many banks don’t offer fixed-rate HELOCs.

It requires a fundamental change in priorities and commitment.

Your household money is typically all smashed together to be more efficient and this can cause potential problems or tensions with spousal spending. Good fences make good neighbors have clear decision making guidelines on how you and your spouse will do this together and tackle any unforeseen challenges or expenses.

Velocity Banking Expert

Ascendant Financial Inc has expert financial advisors and coaches that can help you understand and implement Velocity banking strategies in your life. Register for the Free training so that you can book a time with your own advisor.

Get Access To The Becoming Your Own Banker On-Demand Training

We will not spam, rent or sell your information. By submitting this form, you agree to receive marketing messages from us to the contact information you provide. You can unsubscribe any time.